-

All Forum Categories

-

Followed Discussions

-

Followed Categories

-

Followed People

-

Followed Locations

-

Market News & Data

-

General Info

-

Real Estate Strategies

- House Hacking

- Commercial Real Estate Investing

- BRRRR - Buy, Rehab, Rent, Refinance, Repeat

- Mobile Home Park Investing

- Innovative Strategies

- Multi-Family and Apartment Investing

- Land & New Construction

- Wholesaling

- Rehabbing & House Flipping

-

Short-Term & Vacation Rental Discussions

presented by

- Tax Liens & Mortgage Notes

- Medium-Term Rentals

- Buying & Selling Small Businesses

- Outdoor Hospitality

-

Landlording & Rental Properties

-

Real Estate Professionals

-

Financial, Tax, & Legal

-

Real Estate Classifieds

-

Reviews & Feedback

Velocity Banking / HELOC Checking Acct - It Works (Proof)

Hi, everyone. I wish everyone knew how great this strategy is, so I'm trying to spread the word. I'm not selling anything, just trying to let people know how it works.

When you're paying your mortgage month in and month out, you are paying MOSTLY interest for many years. That's because you are paying interest on the whole loan - $200K @ 4%, let's say. In the first year you'll only bring the balance down about $4K, but you'll pay about $8.5K in interest - twice as much, obviously. To pay the balance down $10K it will take you 2.5 years and over $20K in interest. To me, that's a sickening waste. Check out from Sept to Sept on this pic. Only $4K in principal yet $8.5K in interest. Work it out on bankrate yourself (link at bottom) and you can see how long and how much interest is wasted to pay off $10K from your mortgage. And this should go without saying, but if you're further along in your mortgage then your savings will be less, because you are paying less in interest at that point. This strategy is more suited to someone who is in their first decade of a mortgage.

Now, follow me here. You can take all of your extra money and put it toward your mortgage which will shorten your mortgage and save you on interest. Most people know this. But most people also realize that money is usually tight and many people don't have $400 for an emergency let alone a bunch of extra money to put against their mortgage. Anyway, do that if you want, but there's also another better way to accomplish the same thing.

Here's how it works. You get a HELOC or a PLOC with a reasonable rate. It doesn't have to be 4%, but it also shouldn't be 18% like a credit card. You take a portion of your mortgage ($5-10K, for example) and put it on the HELOC. Then you put all of your income toward the HELOC and try to depress the balance as much as possible all month. When bills come you use HELOC funds to pay them, because you're not putting your income into a checking account anymore. You continue like this, putting all bills and income toward the HELOC balance. Since you make more than you spend, the balance will gradually come down. Then you put another portion of your mortgage on the HELOC and repeat the process.

Here's how and why it works (and works better than just paying extra principal when you have the money):

1. You are putting all of your available "checking" funds toward your mortgage at all times, yet you still have money to pay bills due to the revolving credit line.

2. Money that you DON'T end up using toward bills stays on the mortgage balance permanently, limiting the amount of interest you will pay.

3. Money that you DO end up using toward bills temporarily "leans" on the mortgage balance keeping it down and limiting the amount of interest you will pay.

4. Here's the silver bullet, though, that most people can't fully grasp. On the above mentioned $200K / 4% loan you will pay $144K in interest over 30 years paying by the amortization schedule. For that amount, you might as well have purchased an extra smaller house. But here's the thing - the interest is SCHEDULED, but hasn't been CHARGED TO YOU YET. If you struggle with this idea, imagine that you won the lottery tomorrow and wanted to pay the house off. You'd pay off the balance of your mortgage, but not the balance and all the scheduled interest charges. In other words, the interest can be AVOIDED COMPLETELY by paying the principal back early, but time is of the essence. The more you pay and the faster you do it the better. So, remember above when I explained that it takes a person about $20K in interest to pay down $10K in principal? Well, when you put that $10K on the HELOC, you COMPLETELY AVOID the $20K in corresponding interest payments on the mortgage (like the lottery example, just a smaller amount) and it will cost you about $1000 in interest to pay off on the HELOC. This allows you to save TENS OR HUNDREDS OF THOUSANDS OF DOLLARS simply by adjusting the way you pay it. It's not a scam or a method of gaming the interest rates or anything like that, it's simply a way of paying more efficiently without having thousands of dollars lying around to throw at your mortgage.

5. When you pay these large chunks, your subsequent REGULAR PAYMENTS are also more effective, because your principal / interest ratio is improved by quite a lot. Normally, every month you will pay $1-$2 less toward interest than the previous month, but the month after you take $10K off of the mortgage your regular payment will charge about $30 less toward interest than the previous month - and every month thereafter. So, you are saving all the interest from #4 as explained, but every month you're also paying significantly less toward interest (and more toward principal) than you were before. Each time you take another "chunk" off of the mortgage your regular payments also become that much more efficient.

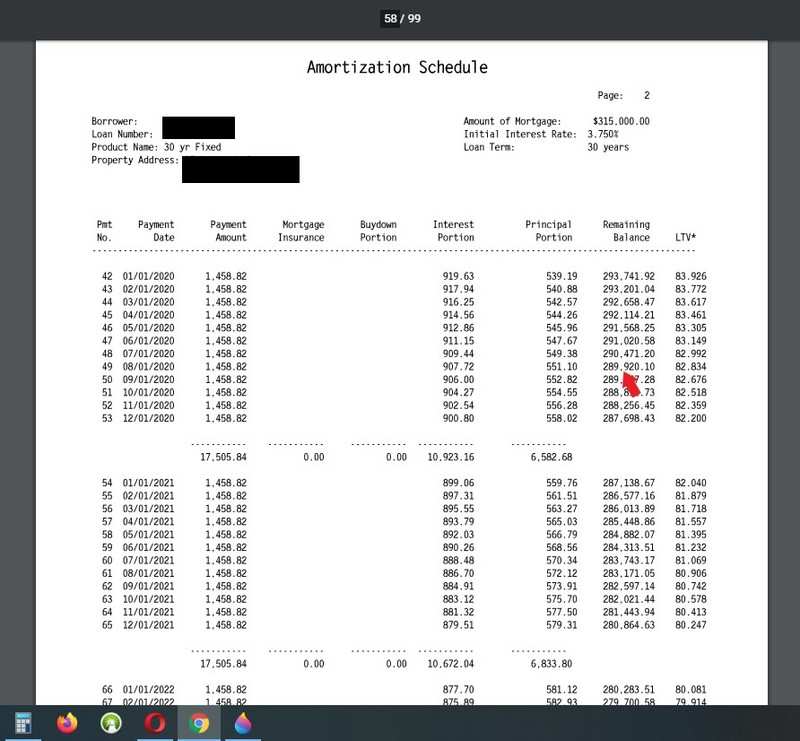

Hopefully, that covers the explanation, but I told you there was proof, so here you go. Here's my closing package where it says that this month I should be at a balance of about $290K.

And here's my actual loan balance of $236.5K. So, as you can see I've been able to put $53.5K extra toward my mortgage over the last two years (started the strategy May 2018) and I haven't been skipping lattes or doing any other financial voodoo. All I have done is started using the HELOC to pay off chunks of the mortgage like I explained and because of all the various mechanisms I described I've been able to put a ton of extra money toward the mortgage. When I look at the balances of $290K and $236K on my closing doc, I find that it is about 85 regular payments (7 years) shaved off the mortgage at an average of $825 interest per month (first payment in range $907 / last payment in range $743). 85 payments at an average of $825/month is $70K worth of interest savings in only two years. Obviously, I have a higher dollar mortgage, so your results may vary, but this isn't milk money, it's life changing money simply from rearranging the way you pay your number one expense. Let me know if you have any thoughts or questions. Thanks!

Originally posted by @Mike S.:

Originally posted by @Joshua S.:Let me present it in another way as obviously I didn't make my message clear.

Let's put the following scenario:

$100k mortgage, 3%, amortized over 30 years. (monthly payment: $421.60)

HELOC, $10k, 4%

Case 1:

Normal amortization of the mortgage without any additional principal payment and no use of the HELOC.

At the end of year 1 your mortgage principal will be down to $97,912 and you would have paid during the year $5,059.25 consisting of $2,087 of principal and $2971 of interest.

payment principal interest balance 1 ($171.60) ($250.00) $99,828.40 2 ($172.03) ($249.57) $99,656.36 3 ($172.46) ($249.14) $99,483.90 4 ($172.89) ($248.71) $99,311.01 5 ($173.33) ($248.28) $99,137.68 6 ($173.76) ($247.84) $98,963.92 7 ($174.19) ($247.41) $98,789.72 8 ($174.63) ($246.97) $98,615.10 9 ($175.07) ($246.54) $98,440.03 10 ($175.50) ($246.10) $98,264.52 11 ($175.94) ($245.66) $98,088.58 12 ($176.38) ($245.22) $97,912.20 ($2,087.80) ($2,971.45) ($5,059.25) Case 2:

Your scenario, taking a 10k HELOC loan, that will be payed back in one year. The HELOC is used to pay the balance down of the mortgage to 90k.

With this scenario, the balance of the mortgage at the end of the year will be $87,608 and you would have payed $2,391 +10,000 of principal and only $2,667 of interest.

However at the same time, you would have paid back $10,000 of principal of your HELOC and $216 of interest.

So, out of pocket you would have to pay $15,275 that year.

mortgage HELOC payment principal interest balance principal interest balance 1 ($196.60) ($225.00) $89,803.40 ($833.33) ($33.33) $9,166.67 2 ($197.09) ($224.51) $89,606.31 ($833.33) ($30.56) $8,333.33 3 ($197.58) ($224.02) $89,408.72 ($833.33) ($27.78) $7,500.00 4 ($198.08) ($223.52) $89,210.65 ($833.33) ($25.00) $6,666.67 5 ($198.57) ($223.03) $89,012.07 ($833.33) ($22.22) $5,833.33 6 ($199.07) ($222.53) $88,813.00 ($833.33) ($19.44) $5,000.00 7 ($199.57) ($222.03) $88,613.44 ($833.33) ($16.67) $4,166.67 8 ($200.07) ($221.53) $88,413.37 ($833.33) ($13.89) $3,333.33 9 ($200.57) ($221.03) $88,212.80 ($833.33) ($11.11) $2,500.00 10 ($201.07) ($220.53) $88,011.73 ($833.33) ($8.33) $1,666.67 11 ($201.57) ($220.03) $87,810.16 ($833.33) ($5.56) $833.33 12 ($202.07) ($219.53) $87,608.09 ($833.33) ($2.78) $0.00 ($2,391.91) ($2,667.29) ($10,000.00) ($216.67) ($15,275.87) Case 3:

Instead of using the HELOC, you use the same $15,275 than in scenario 2, but you use it spread over 12 months to make additional payment to your mortgage.

At the end of the year you mortgage balance will be $87,555. Better than in case 2.

payment principal interest balance 1 ($1,022.89) ($250.00) $98,977.11 2 ($1,025.45) ($247.44) $97,951.66 3 ($1,028.01) ($244.88) $96,923.65 4 ($1,030.58) ($242.31) $95,893.07 5 ($1,033.16) ($239.73) $94,859.91 6 ($1,035.74) ($237.15) $93,824.17 7 ($1,038.33) ($234.56) $92,785.84 8 ($1,040.93) ($231.96) $91,744.92 9 ($1,043.53) ($229.36) $90,701.39 10 ($1,046.14) ($226.75) $89,655.25 11 ($1,048.75) ($224.14) $88,606.50 12 ($1,051.37) ($221.52) $87,555.13 ($12,444.87) ($2,829.81) ($15,274.68)

Sorry, Mike. I know all this, but you're not looking at the total cost, which is more important.

1. Just paying extra principal is not part of the discussion. Most people don't have a ton of extra money lying around - they are looking for other ways to go about things. This strategy works for someone who has very little disposable income. Simply paying additional principal does not. Most people don't even have $400 saved up for an emergency, so they aren't paying extra principal, but that CAN do this strategy without an extra outlay because they're simply shifting debt from one place to another and paying it differently.

2. Total interest charges paying off the $10K on the bank's schedule: $13K over 5 years.

3. Total interest charges paying off the $10K on the HELOC: $1K over 1 year.

That's it. Those are the real world facts in this scenario that matter, not what rate you're paying and so on. You're not talking apples to apples. Line up your mortgage numbers on an amortization calculator and put in an extra $10K payment and see how much interest it would save you. Then calculate how much it would cost you to pay off on a HELOC where all of your income goes toward it. Those are the only two numbers that matter - how much you save and how much it costs to do it. Unless you want to talk apples, you might as well tell me who your favorite girl bands are, because we're having two different discussions. I always liked The Breeders.

Originally posted by @Joshua S.:1. Just paying extra principal is not part of the discussion. Most people don't have a ton of extra money lying around - they are looking for other ways to go about things. This strategy works for someone who has very little disposable income. Simply paying additional principal does not. Most people don't even have $400 saved up for an emergency, so they aren't paying extra principal, but that CAN do this strategy without an extra outlay because they're simply shifting debt from one place to another and paying it differently.

No it does not, if you don't pay back the principal of the HELOC, you are paying more interest on the HELOC that you were paying on the mortgage. You seem to forget that the interest that you pay to your HELOC is in addition to the mortgage. So you are paying more every month.

The way you describe it, you need even more cash to pay back the HELOC principal. The only thing that you do, is that you borrow from the HELOC to go to the mortgage. As long as you don't pay back the money that you borrow, you will have to pay interest. And the interest on the HELOC is usually higher than on the mortgage.

As I demonstrated before, you will get ahead if you would put that additional money directly into the mortgage principal instead of using a HELOC.

Velocity banking is fine for people who can't budget as it give them a plan to follow and force them to save more. But you can do better without using the HELOC and paying directly more into the mortgage.

Originally posted by @Mike S.:Originally posted by @Joshua S.:1. Just paying extra principal is not part of the discussion. Most people don't have a ton of extra money lying around - they are looking for other ways to go about things. This strategy works for someone who has very little disposable income. Simply paying additional principal does not. Most people don't even have $400 saved up for an emergency, so they aren't paying extra principal, but that CAN do this strategy without an extra outlay because they're simply shifting debt from one place to another and paying it differently.

No it does not, if you don't pay back the principal of the HELOC, you are paying more interest on the HELOC that you were paying on the mortgage. You seem to forget that the interest that you pay to your HELOC is in addition to the mortgage. So you are paying more every month.

The way you describe it, you need even more cash to pay back the HELOC principal. The only thing that you do, is that you borrow from the HELOC to go to the mortgage. As long as you don't pay back the money that you borrow, you will have to pay interest. And the interest on the HELOC is usually higher than on the mortgage.

As I demonstrated before, you will get ahead if you would put that additional money directly into the mortgage principal instead of using a HELOC.

Velocity banking is fine for people who can't budget as it give them a plan to follow and force them to save more. But you can do better without using the HELOC and paying directly more into the mortgage.

Awesome, now we're getting somewhere. You have a fundamental misunderstanding of the strategy, so if you're willing to listen, I can clear it up for you.

You're not putting the money on the HELOC and letting it sit there, you're basically using the HELOC like a checking account. At the start of the month you have $90K on your mortgage and $10K on the HELOC. Then in a week or two you get paid and the HELOC goes down to $7000. A couple more weeks go by and you get paid again so you are at $4000, but you also get your regular bills - mortgage, car, electric, water, phone, etc. and your balance goes back up to $9000. For the full month, you paid off $1000 total, but your income also held down your average daily balance to $7000, let's say. So, instead of paying interest on the entire $10K, you pay interest based on $7000. Then as you repeat this every month, your HELOC balance dwindles (because you make more than you spend), but you are only paying interest based on the average daily balance each month, which is less than the $10K, because your income is holding it down temporarily. That's the strategy. I don't know where you got the idea that you just let the HELOC sit there, that's contrary to the entire point of what you're doing. The strategy is that you're essentially using the HELOC like an inverse checking account. Income goes in, bills come out. At the end of the month the balance should be less AND throughout the month the balance was being held down by your income while you were waiting for bills. When you're talking about 'just paying extra principal', most people don't have the money for that, as I said, AND doing that won't hold your mortgage balance down temporarily while you wait for bills.

People don't realize it, but you pay your mortgage based on the average daily balance. The problem is that you can't put all of your income toward your mortgage to hold your ADB down and then get it back out to pay your bills. That's why you use a HELOC to accomplish the same thing. You sort of "install" this small portion of your mortgage that you CAN put all your money toward and then get it back when you need it. And whatever is left over automatically stays on the mortgage every month, so it works both ways. If your car breaks down or whatever maybe your balance doesn't go down that month, but you'll always be in a better position than if your money was sitting in a checking account doing nothing. And remember, all of this is going on while you're still paying your regular mortgage payments, but because you paid early principal your principal / interest ratio next month goes from $172.03/$249.57 to $197.03/$224.57 and your regular payments are putting more toward principal, too. Every month you're able to keep $25 more dollars in your pocket instead of spending it to interest and you've shortened your mortgage by years just by changing the way you pay.

So, look. I'm the case study and I'm telling you flat out that even at 8% or whatever my crappy rate is, I STILL only pay $1000/year ($83/month) to do this whole thing and I'm not even great at it. But this is why I've been telling you to focus on the cost vs return - imagine someone wanted to give you $13K (lottery, gift, whatever), but you had to buy a $1000 plane ticket to go pick it up. Would you turn it down because there's a cost involved? No, any idiot can see that it's well worth the $1000 plane ticket to go get 13x that much. That's what I'm doing here. I'm paying about $1000 each year to put around an extra $20K/year on my mortgage, which saves me a ton on interest. In your example, it's the $13K savings, but my mortgage is over twice that large at this point, so my savings probably dwarf that and I'm also shortening my mortgage by years. The cost of the HELOC is more than covered by what I'm saving, that's why it's a non-issue. Of course if I was just taking a portion of my mortgage and putting it on a HELOC and letting it sit there, then you can assume I'm just paying more interest toward the HELOC than I would have toward the mortgage, but that's not what we're talking about. The bottom line is that I'm saving a ton of money by keeping all of my income focused on my mortgage and it costs me $83/month to do it. I know people that spend that on getting their cars detailed. It's nothing compared to what I'm saving. This makes more sense, right?

@Joshua Smith

You are not only paying interest on the HELOC. You are also paying Principal...

Count all the money that you you are putting in your HELOC and you will see that if you were putting all that money in your mortgage instead you would be ahead.

But obviously you don't understand that. Wherever the loan is coming from it is still a loan that accrues interest. You are paying the interest. And HELOC rate are usually more expensive than mortgage. You are just playing with the time difference between when you get your salary until when you pay your bills. You are basically removing the cushion of a savings account and using the HELOC instead as your bank account. That part I agree saves money but is dangerous as HELOC can and have been frozen by banks.

I am glad that this system is working for you and making you better at saving money. That’s the whole point and you seem to be an excellent candidate for this system.

Good luck in your endeavors.

Before this thread becomes 69 pages long like an earlier thread on more or less the same topic (see link below), I'll quote @Steve Vaughan from that same thread, who asked @Joshua S.: "Don't you have a higher rate or crappier term loan to go after? If the loan getting punched in the face had a higher rate, I think the whole idea would be better received. Yet these 27 pages or whatever are only about paying down a 3% loan".

Yes, that's right. I thought the arguments being pursued by Joshua in this thread sounded all too familiar, and it seems the intervening two years have done nothing to dim his enthusiasm to borrow money at higher interest to partially pay off a low Interest Rate mortgage, even though mortgage Interest Rates are even lower now than then. So, I suspect his "whole idea" should be even less well received now, per Steve's pearl of wisdom two years ago.

Here's the link: https://www.biggerpockets.com/...

Perhaps read both sides of the argument there, before reinventing the wheel here?...

Originally posted by @Mike S.:@Joshua Smith

You are not only paying interest on the HELOC. You are also paying Principal...

Count all the money that you you are putting in your HELOC and you will see that if you were putting all that money in your mortgage instead you would be ahead.

But obviously you don't understand that. Wherever the loan is coming from it is still a loan that accrues interest. You are paying the interest. And HELOC rate are usually more expensive than mortgage. You are just playing with the time difference between when you get your salary until when you pay your bills. You are basically removing the cushion of a savings account and using the HELOC instead as your bank account. That part I agree saves money but is dangerous as HELOC can and have been frozen by banks.

I am glad that this system is working for you and making you better at saving money. That’s the whole point and you seem to be an excellent candidate for this system.

Good luck in your endeavors.

Yes, I know I'm paying principal. I've been explaining that over and over. That's the whole point of a mortgage whether it's a fixed first or a HELOC. What I have been saying is that my "cost" is $1000/year worth of interest on the HELOC. Pretty funny that you're saying I'm the one who doesn't understand. LOL

Good luck to you, too!

Originally posted by @Joshua S.:

Yes, I know I'm paying principal. I've been explaining that over and over. That's the whole point of a mortgage whether it's a fixed first or a HELOC. What I have been saying is that my "cost" is $1000/year worth of interest on the HELOC. Pretty funny that you're saying I'm the one who doesn't understand. LOLGood luck to you, too!

You are not consistent. You are saying that you don't have extra money to pay the principal on your mortgage and that is why you are using a HELOC, but you don't consider that you have the money to pay the principal back on your HELOC...

Originally posted by @Brent Coombs:Before this thread becomes 69 pages long like an earlier thread on more or less the same topic (see link below), I'll quote @Steve Vaughan from that same thread, who asked @Joshua S.: "Don't you have a higher rate or crappier term loan to go after? If the loan getting punched in the face had a higher rate, I think the whole idea would be better received. Yet these 27 pages or whatever are only about paying down a 3% loan".

Yes, that's right. I thought the arguments being pursued by Joshua in this thread sounded all too familiar, and it seems the intervening two years have done nothing to dim his enthusiasm to borrow money at higher interest to partially pay off a low Interest Rate mortgage, even though mortgage Interest Rates are even lower now than then. So, I suspect his "whole idea" should be even less well received now, per Steve's pearl of wisdom two years ago.

Here's the link: https://www.biggerpockets.com/...

Perhaps read both sides of the argument there, before reinventing the wheel here?...

Yes, feel free to read about all the theories and ideas elsewhere and then when you want proof that it works you can come to this thread and see all my updates with statements and stuff. That's a good idea. I mean, I'm showing everyone my amortization schedule and my latest statement so they can see my current balance and how different it is from where I should be. You can beat the ideas all to death and talk in circles about what you "think" is wrong with the idea, but I'm actually doing it and I'm offering proof. How would you suggest that I paid an extra $58K toward my mortgage over the last three years, btw, if it's not the strategy working? Did I win the lottery and somehow not notice? Am I independently wealthy and very forgetful? Did my wife and I get $60K worth of raises and then get hit in the head with paint cans by Macaulay Culkin or something? Let me know how you think this could have happened, I'm super interested in your theory.

Go look at my amo table and my statement a couple pages back and you can see a $58K difference. That's all I'm trying to provide here - my experience with it and proof that it works. If you're not interested that's great, you're welcome to blindly criticize or kiss off or whatever you want to do. Other people might look at the proof I'm providing and realize that it holds more weight than what people "think" will happen, so I'm posting for anyone who might be into that. So, yeah, you could call it reinventing the wheel to offer proof that I'm doing it and how well it works instead of offering words and spreadsheets about what I think would happen. I like it. Reinventing the wheel, that's me. LOL

Anyway, please, PLEASE let me know your theory on how I came up with an extra $58 grand, though, because if it wasn't through this strategy, I'm going to need your help to figure out how to do it again! Thanks.

Originally posted by @Mike S.:Originally posted by @Joshua S.:

Yes, I know I'm paying principal. I've been explaining that over and over. That's the whole point of a mortgage whether it's a fixed first or a HELOC. What I have been saying is that my "cost" is $1000/year worth of interest on the HELOC. Pretty funny that you're saying I'm the one who doesn't understand. LOLGood luck to you, too!

You are not consistent. You are saying that you don't have extra money to pay the principal on your mortgage and that is why you are using a HELOC, but you don't consider that you have the money to pay the principal back on your HELOC...

Ok, I think I see the problem.

Scenario 1: "Man, I wish I could put more against my mortgage, but I usually only have a couple hundred or a thousand left over in checking at the end of the month and I don't want to tie that up where I can't get it back in case something comes up."

Scenario 2: "I'm so glad that I use this HELOC checking account strategy, because it allows me to put all of my income against my mortgage. Even though I only have a few hundred or a thousand left over at the end of each month (same as above), it all goes toward my mortgage and I can still take it out if something comes up, so it's the best of both worlds."

Can you see a difference between those two things? You're not "paying down" the HELOC, you're putting all of your money toward it every month and paying your bills out of it every month. Assuming that you make more than you spend, it naturally comes down over the course of the year. The so-called "EXTRA" money can be a very small amount, but still go toward the mortgage in this strategy whereas a person with a very small amount left over in their normal checking account isn't going to throw that at the mortgage. The strategy allows you the freedom of putting all of your income toward the mortgage without having to worry about leaving yourself short.

I'd rather use my HELOCs to buy rentals than pay down 30 year fixed rate debt at 3-5% interest :)

For a single home owner maybe it’s good

For me I want to borrow as much money as possible and keep it as long as I can

Returns are 100 - 200% so paying 4 or even 10% interest is not a factor for me

Originally posted by @Max T.:I'd rather use my HELOCs to buy rentals than pay down 30 year fixed rate debt at 3-5% interest :)

I'm confused about your use of the term "rather". Taking a $10K chunk of one of my HELOCs or my PLOC and using it to pay down my primary residence faster doesn't stop me from buying rentals. If you can only do one or the other you got bigger problems to worry about. :-D

Originally posted by @Michael Plante:For a single home owner maybe it’s good

For me I want to borrow as much money as possible and keep it as long as I can

Returns are 100 - 200% so paying 4 or even 10% interest is not a factor for me

Again, this isn't an investment or in place of an investment. It's simply a better way to run your checking and makes your money work for you constantly instead of sitting around waiting for you to do something with it.

Originally posted by @Joshua S.:Originally posted by @Michael Plante:For a single home owner maybe it’s good

For me I want to borrow as much money as possible and keep it as long as I can

Returns are 100 - 200% so paying 4 or even 10% interest is not a factor for me

Again, this isn't an investment or in place of an investment. It's simply a better way to run your checking and makes your money work for you constantly instead of sitting around waiting for you to do something with it.

Guess I’m not understanding like others in the thread

I never have money sitting around

I malways looking for more to invest

Originally posted by @Joshua S.:Originally posted by @Max T.:I'd rather use my HELOCs to buy rentals than pay down 30 year fixed rate debt at 3-5% interest :)

I'm confused about your use of the term "rather". Taking a $10K chunk of one of my HELOCs or my PLOC and using it to pay down my primary residence faster doesn't stop me from buying rentals. If you can only do one or the other you got bigger problems to worry about. :-D

It is the opportunity cost brotha man. I could do it but why? I want as many cash flowing units as possible on that sweet sweet 30 yr fixed sub 5% debt. Paying down debt on my primary rez does not make progress toward those goals. A free and clear primary residence is just dead equity at this point in my journey. I'm not interested in paying off cheap money with interest only variable rate debt. Maybe when I'm an ol' head exiting the growth phase I'll start caring about paying them down, but I'll do that with cash flow not borrowed money.

This is bonkers, I can't believe I'm the only person who gets this. Listen, everybody.

I have rentals.

I have stocks.

I have emergency savings.

I'm not advocating doing this HELOC strategy in place of any of those things. I don't understand how I can make that any clearer.

But here's something you have that I don't want: a checking account where your money is sitting there rotting while you wait to pay your bills.

Instead, I have used this method to put all my CHECKING ACCOUNT FUNDS (ie. the money you have rotting in your checking account right now) plus a portion of a line of credit against my mortgage. Everyone agrees that paying extra principal saves you money on interest. I'm not selling my current rentals or foregoing buying others to do it. I'm not selling my stocks to do it. I'm not using my emergency savings to do it. I'm simply using my checking account and a line of credit to do it. The whole process costs about $83/month in interest on the HELOC and I've saved tens of thousands of dollars doing it.

People keep saying that they'd rather invest the money than do what I'm doing. Awesome. Then what is your checking account balance right now? It should be zero if you'd rather invest the money, so who's got the first screen shot of their checking account with a zero balance, because it's all invested somewhere? Let me know!

Originally posted by @Michael Plante:Originally posted by @Joshua S.:Originally posted by @Michael Plante:For a single home owner maybe it’s good

For me I want to borrow as much money as possible and keep it as long as I can

Returns are 100 - 200% so paying 4 or even 10% interest is not a factor for me

Again, this isn't an investment or in place of an investment. It's simply a better way to run your checking and makes your money work for you constantly instead of sitting around waiting for you to do something with it.

Guess I’m not understanding like others in the thread

I never have money sitting around

I malways looking for more to invest

Refer to the other comment I just made - If all of your money is working for you right now, what is your checking account balance? Zero, correct?

Originally posted by @Max T.:Originally posted by @Joshua S.:Originally posted by @Max T.:I'd rather use my HELOCs to buy rentals than pay down 30 year fixed rate debt at 3-5% interest :)

I'm confused about your use of the term "rather". Taking a $10K chunk of one of my HELOCs or my PLOC and using it to pay down my primary residence faster doesn't stop me from buying rentals. If you can only do one or the other you got bigger problems to worry about. :-D

It is the opportunity cost brotha man. I could do it but why? I want as many cash flowing units as possible on that sweet sweet 30 yr fixed sub 5% debt. Paying down debt on my primary rez does not make progress toward those goals. A free and clear primary residence is just dead equity at this point in my journey. I'm not interested in paying off cheap money with interest only variable rate debt. Maybe when I'm an ol' head exiting the growth phase I'll start caring about paying them down, but I'll do that with cash flow not borrowed money.

The opportunity cost is attached to the money in your checking account that's not working for you right now. I'm not foregoing rentals, stocks, etc., I'm simply making sure all my money is working for me by putting it against my mortgage in a line of credit. That sweet sweet sub 5% ends up costing a total of around 67% interest if you pay it off over 30 years and I've got my checking account funds leaning on it to bring it down. What is your checking account doing for you?

@Joshua S., you wrote: "That sweet sweet sub 5% ends up costing a total of around 67% interest if you pay it off over 30 years", as if that's a bad thing(?)

My mortgage calculator tells me that if I have a 3% Interest Rate for thirty years, I'm only paying 52% interest, in total. (Meanwhile, my primary increased in value by more than 1,000% over the same period of time).

I'll take that deal every time.

But if, like that fellow in Hawaii, we're all able to get the same terms and Interest Rate on a HELOC instead of a "normal" mortgage, then sure, why not have all our income and all our expenses going to and from our one loan account?

But, for those whose expenses often exceed their income in any given month, and are tight every other month, there will be no "velocity" of debt reduction.

That's all.

Originally posted by @Brent Coombs:@Joshua S., you wrote: "That sweet sweet sub 5% ends up costing a total of around 67% interest if you pay it off over 30 years", as if that's a bad thing(?)

My mortgage calculator tells me that if I have a 3% Interest Rate for thirty years, I'm only paying 52% interest, in total. (Meanwhile, my primary increased in value by more than 1,000% over the same period of time).

I'll take that deal every time.

But if, like that fellow in Hawaii, we're all able to get the same terms and Interest Rate on a HELOC instead of a "normal" mortgage, then sure, why not have all our income and all our expenses going to and from our one loan account?

But, for those whose expenses often exceed their income in any given month, and are tight every other month, there will be no "velocity" of debt reduction.

That's all.

I have to give you guys credit, you have been able to spin the same ridiculous argument a thousand different ways.

If your primary increases by 1000% and you pay 52% interest, that's great.

If your primary increases by 1000% and you pay 26% interest, that's better.

You could put your checking account funds to use and be in an even better position, but you don't want to and that's cool. Some people like leaving money on the table. Some people give to charities, you like to give to banks. It's not how I like to roll, but to each his own. Have a good one.

Here's a summary of this thread for anyone else who wants to play.

Me: "Hey, this is pretty cool. I found a way that a person can put their checking account funds to use instead of just letting the money sit there like you're all doing right now."

You: "But I don't want to sell my rentals and stocks and stuff."

Me:

LOL

- Lender

- The Woodlands, TX

@Brent Coombs. One of the issues in the “calculations” of the “velocity” believers is that they do no accounting for the time value of money. They just quote interest savings of say $10,000. And it only cost them $4,000. But that $4,000 needs to be invested now, in order to save $10,000 25 years from now.

The second issue is the argument put forth by the velocity worshippers that before using a HELOC for everyday spending they had no idea where their money went or what it was spend on; now with the HELOC their personal living expenses are far less, they purchase far fewer consumables, and hence their savings rate, to be invested in paying down the mortgage is much higher. Have these guys ever heard of Quicken or any of the online personal finance programs available to track spending?

It has occurred to me that the velocity believers actually somehow believe that the world of economics has been altered, and paying 4% interest to pay down a 3% mortgage is somehow profitable. Obviously what some of them have done is decrease consumer spending and increase savings. This of course could have been accomplished without the need of using negative interest rate leverage.

I also find it interesting that for some velocity believers a simple (flawed) personal finance strategy has taken on a cult like worship. These people have a them vs us view of the world very similar to the cult believers. It’s no longer a matter of doing a correct financial analysis; it’s now tied in to banks tricking you with “front loaded interest”, the evils of tying you in to “30 year mortgages”, being a “debt slave”.

Full disclosure, I've actually done something similar to this/am doing this now. I purchased a property 5-6 years ago and then 2-3 years ago took out a HELOC to payoff the remaining mortgage and am now paying off the HELOC (I actually had it paid off last year but then used the HELOC to purchase another property and am now paying it back down). Bottom line, it can be an effective strategy in that it can save you money in interest (compared to paying it out over the full term of the loan) and yes can quickly increase your equity in your property compared to a conventional mortgage. The other advantage that the original poster hasn't mentioned is the HELOC is simple interest that is calculated monthly. Every time you pay down that part of that balance, the amount of interest that is calculated for the next month decreases.

That said, you really need to ask yourself what your goals are. Are you going to hold the property forever? 30-50 years? Or are you possibly going to sell it in 5-10 years? If you're going to sell it in 5-10 years then this becomes an appealing strategy because of the additional principal balance you will have paid down during that shorter time period. If you're going to hold the property forever then there's probably more effective ways of using your wealth to either purchase more properties or invest wisely. It really comes down to what is your comfort level with debt? Some people hate it and want to get out of it as quickly as possible, others love it and want to use it to increase their assets. I can see that evidenced by just the ones who responded in this thread. :)

Originally posted by @Don Konipol:@Brent Coombs. One of the issues in the “calculations” of the “velocity” believers is that they do no accounting for the time value of money. They just quote interest savings of say $10,000. And it only cost them $4,000. But that $4,000 needs to be invested now, in order to save $10,000 25 years from now.

The second issue is the argument put forth by the velocity worshippers that before using a HELOC for everyday spending they had no idea where their money went or what it was spend on; now with the HELOC their personal living expenses are far less, they purchase far fewer consumables, and hence their savings rate, to be invested in paying down the mortgage is much higher. Have these guys ever heard of Quicken or any of the online personal finance programs available to track spending?

It has occurred to me that the velocity believers actually somehow believe that the world of economics has been altered, and paying 4% interest to pay down a 3% mortgage is somehow profitable. Obviously what some of them have done is decrease consumer spending and increase savings. This of course could have been accomplished without the need of using negative interest rate leverage.

I also find it interesting that for some velocity believers a simple (flawed) personal finance strategy has taken on a cult like worship. These people have a them vs us view of the world very similar to the cult believers. It’s no longer a matter of doing a correct financial analysis; it’s now tied in to banks tricking you with “front loaded interest”, the evils of tying you in to “30 year mortgages”, being a “debt slave”.

It's interesting, earlier on in this process I did think it was a bit nefarious of the banks to "charge more interest up front", but now I understand that it's just a function of how much you owe. However, just because it's not nefarious or morally wrong doesn't mean it isn't true. To pay down the first $10K on a $200K / 4% mortgage it costs you over $20K in interest and takes over 2 years. Or looking at it another way, you pay about $11,500 in total payments in the first year and about $8000 of that goes to interest. That means your ACTUAL interest cost in the first year comes to 69% of what you pay. Again, it's not a nefarious, evil thing, but you do, in fact, pay way more to interest in the first years of a mortgage. I find that very wasteful.

On the other hand, I can isolate that top $10K off of my mortgage and because I'm putting all of my income toward it (and not paying interest on the rest of the mortgage while I do it) it costs me around $1000 in interest and takes less than a year. I don't understand how people can look at the difference between $20K and $1K and shrug it off. Go look at my amortization table and my latest statement a couple pages back - I'm $58K ahead of schedule. Where did I come up with that kind of cash? You think I skipped enough Starbucks to save that up, I guess, which is a little far fetched especially if you knew my wife's spending habits.

Lastly, you talk about the time value of money, but I have investments (rentals, stocks, etc.) and emergency savings. I'm using the money that would have been sitting in my checking account to do this, so all of my money is working for me. I'm sure you have money sitting in a checking account right now, so what's the opportunity cost of letting that money sit there? How much could you save or earn off of that if you had a way to make it work for you? You're worried about the time value of money for someone who's doing a strategy like this, but your money is just sitting there, so aren't you calling the kettle black?

Part of the problem here is that fundamentally people don't understand what happens when you pay extra principal (ie. pay it back early) and I think that's a terrible, ridiculous shame, so here's a little experiment for anyone who's interested.

Go to this calculator at put in a $10K loan at 4%. Leave the 30 years. Let's imagine it's a car loan for 30 years.

https://www.bankrate.com/calcu...

Here's what it looks like if you don't feel like doing it.

You pay about $50/month and early on about $33 of that goes to interest. Over the 30 years you pay about $7200 worth of interest, which is obviously 72% interest total.

Now imagine you set this all up, but then tax time comes around and you get a $10K refund, so you figure let's knock out some debt. You pay the $10K off in full. When you do that, it LITERALLY 100% CANCELS the interest that you were scheduled to pay. In other words, the bank isn't going to continue charging you for the $7200. Everyone knows this.

But here's the thing: Regardless of how much you pay, paying early principal LITERALLY 100% CANCELS the corresponding interest.

So, think about your mortgage. You know that every month early on you are paying far more in interest. On the average $200K mortgage, the interest that corresponds to the first $10K of principal is over $20K. That means if you give them $10K early, it LITERALLY 100% CANCELS $20K worth of interest. This is true whether someone gives you a gift or if you win a scratch off ticket or you take it from a HELOC. The difference with a HELOC is that I pay about $1000/year ($83/month) to do it.

So, the question is - is it worth $1000/year to save $20K in interest? Obviously it is.

Now as my balance goes down my savings will go down, because obviously the less there is to save the less I will save. But either way, I'm still always in a winning position by keep all my checking funds working for me all the time.

I hope people can get this, because knowing that paying extra principal saves money, but not understanding how it works is really a shame.