Opportunity Fund or 1031 Exchange: Which is better?

The 1031 Exchange has been one of the most tax efficient investment vehicles available to real estate investors for many years. However, with the creation of Opportunity Funds under the Opportunity Zone program, the 1031 Exchange is being given a well-deserved run for its money. That’s because Opportunity Funds not only offer investors the ability to defer and reduce their initial capital gains tax bill, they also offer a way to eliminate any capital gains taxes earned from their Opportunity Fund investments under certain conditions.

A Review of Opportunity Funds and the 1031 Exchange

1031 Exchanges (or like-kind exchanges) allow investors to defer paying capital gains tax on the sale of a property by reinvesting proceeds into a new property. This process is sometimes called “swapping”. A 1031 Exchange allows an investor to preserve the gross equity earned from a real estate investment, which increases their buying power.

Opportunity Funds are investment vehicles that aim to invest at least 90% of their capital into Qualified Opportunity Zones. By investing in Opportunity Zones through a Qualified Opportunity Fund, investors may be able to defer paying capital gains tax on an appreciated asset sale until 2027. They may also be able to reduce their original capital gains tax liability by up to 15%, and possibly avoid paying any tax on gains from their Opportunity Fund investment.

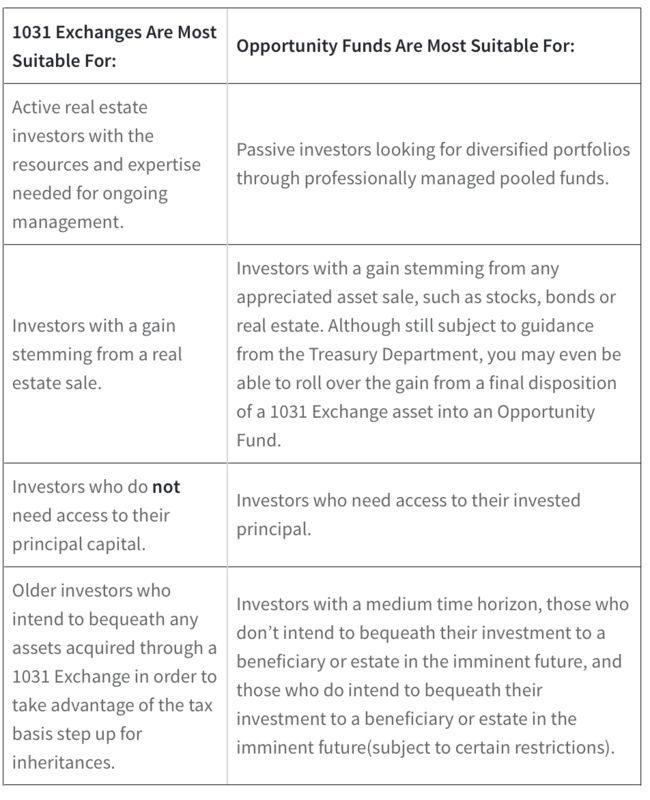

Differences Between Opportunity Funds and the 1031 Exchange

Before going into detail, let’s look at a high-level side-by-side comparison of these two investment options:

Which One offers the Most Advantages to Investors?

Let’s look at each component of the investment options in more detail to determine which one offers the greatest tax advantages for investors.

Rollover

To conduct a 1031 Exchange, investors must reinvest both the principal and capital gain proceeds from the sale of an appreciated asset within 180 days of sale. A 1031 Exchange is technically a “swap” of one property for another, rather than engagement in a pure sale, which would normally constitute a taxable event.

That said, finding an investor to swap properties with can be infeasible in terms of practicality. Because of that, the IRS also allows for something known as a non-simultaneous or “Starker” exchange. Under this like-kind exchange, an investor sells a property, and then purchases another property of “like kind” within 180 days of the sale (or by the day that their next tax bill is due) through a qualified intermediary. Starker exchanges are most common type of exchange, because of the logistical difficulty involved with finding a suitable match for a swap.

Unlike 1031 Exchanges, Opportunity Funds require investors to reinvest onlytheir capital gain within 180 days in order to qualify for tax benefits. There are no requirements regarding the principal of the initial investment.

Also unlike 1031 Exchanges, investors can invest in Opportunity Funds directly, and are not required to go through an intermediary. In order to qualify for the tax advantages of Opportunity Funds, investors are only required to indicate on their income tax return that they rolled their capital gain into an Opportunity Fund. Since Opportunity Fund investments don’t require a middleman intermediary, the buying and selling process can be more streamlined, which can reduce transaction costs and fees for investors.

Qualified Assets

Real estate is the only asset that qualifies for 1031 Exchanges. That means that an investor can defer capital gains tax payments by conducting a 1031 Exchange for the sale of a property, but not for the sale of any other kind of appreciated asset such as stocks or bonds.

While a 1031 Exchange may be a useful option for those seeking to defer capital gains tax payments indefinitely, an Opportunity Fund offers investors a way to defer and reduce capital gains tax liability for both real estate and non-real estate investments – but for a finite amount of time.

On top of allowing an investor to defer and reduce capital gains tax from the sale of multiple types of assets, Opportunity Funds themselves can invest in multiple types of assets. They can be used to invest not only in real estate, but also in company stock, business partnership interests, and in capital resources such as factory equipment. Overall, in terms of asset options, Opportunity Funds offer investors a greater number of choices and diversification potential than 1031 Exchanges.

But, it’s worth noting that Opportunity Funds must also adhere to restrictions regarding the types of real estate assets that can be included within the funds. Since the Opportunity Zone program is intended to incentivize investment in economically distressed areas, the assets must be physically located in Opportunity Zone communities.

Additionally, Opportunity Funds may only invest in real estate assets if the original use of the property commences with the Opportunity Fund, or the asset is substantially improved. In practical terms, this generally limits investments to new construction or redevelopment projects. This strategy can be useful for long-term investors focused on maximizing appreciation potential, but it also requires significant experience and operational expertise on the part of the Opportunity Fund manager.

Investment Structure

As mentioned previously, because they were originally created to swap properties, 1031 Exchanges are generally useful for selling a single asset in exchange for another single asset. There are ways around the single asset structure, but navigating the process is very complex and usually comes with relatively high transaction costs.

Opportunity Funds, on the other hand, can be structured as pooled funds. By pooling funds from multiple investors, investors can acquire a diversified portfolioof real estate (and possibly other) assets, rather than a single building. This is a key differentiator, because diversification inherently reduces the risk of an investment portfolio.

Additionally, with an Opportunity Fund investment, the work of acquiring and managing assets doesn’t fall on the shoulders of the investor, but on the fund manager. While 1031 Exchanges can offer advantages for experienced real estate operators who want the hands-on management of assets for many years, Opportunity Funds offer a way for more passive investors to potentially benefit from significant tax incentives.

Capital Gains Tax Deferral

One benefit of1031 Exchanges over Opportunity Funds is the ability to defer capital gains tax payments indefinitely. An investor could conduct a series of rollovers, swapping Property A for Property B, then Property B for Property C, and so on while deferring any capital gains tax liability for years or even decades until they eventually dispose of an asset either through a traditional sale or through inheritance and estate planning.

Opportunity Fund investments allow investors to defer paying capital gains tax on their initial realized capital gains, but unlike a 1031 Exchange, that tax bill has set due date. Taxes on this capital gain will be due in 2027, or when the Opportunity Fund investment is sold – whichever happens first.

But, investors who conduct a series of 1031 Exchanges will face other issues, such as depreciation recapture. When an asset is disposed of, any depreciation deductions claimed for that asset in previous tax filings may potentially be taxed as ordinary income or a special capital gains rate, depending on the depreciation method used. While recaptured section 1250 gains (i.e., depreciation claims taxable as ordinary income upon disposition of an asset) are not expected to be eligible for a rollover into an Opportunity Fund, unrecaptured section 1250 gains (i.e., those taxable at the 25%capital gains rate) are expected to be eligible, hence enabling investors to potentially defer and reduce their capital gains tax liability.

On top of this, investors may have difficulty finding a suitable replacement asset that will help them avoid additional taxes. To the extent that an investor receives cash or other property that is not of like-kind (otherwise known as a “boot”), the investor will realize a taxable gain. A boot can also arise from the differential amount in the equity or debt of the asset being disposed of and the one being acquired. By contrast, with Opportunity Fund investments, an investor can tailor the amount invested to correspond with the exact amount of any capital gains they have realized within the past 180 days.

Capital Gains Tax Reduction

An Opportunity Fund offers access to a “step up” in an investor’s tax basis. This gives investors the ability to defer paying capital gains taxes on their initial gain and reduce their tax bill when it comes due.

If you hold your Opportunity Fund investment for at least 5 years, you can step up your initial cost basis and reduce your capital gains tax liability by 10%. If you hold your investment for at least 7 years, you can step up your basis to reduce your capital gains tax liability by 15% in total. However, this tax benefit runs out on December 31, 2026, at which point the original capital gains tax bill is triggered, with the tax liability being due in 2027.

A 1031 Exchange, on the other hand, can help a real estate investor defer capital gains, it can’t help an investor reduce capital gains owed. A tax basis step-up is only possible for inheritances.

Tax Upon Sale

Under the 1031 Exchange, investors will eventually be taxed on their capital gains in full upon their final disposition – assuming that the disposition happens while the investor is living. This means that if the last asset acquired in a series of 1031 Exchange rollovers appreciates significantly, when that asset is divested the investor (or their estate) could incur a sizable tax bill.

In contrast, Opportunity Fund investors can expect permanent exclusion for any gains realized on their initial qualifying investment in the Opportunity Fund if they hold the investment for at least 10 years. In other words, even if the investor realizes a sizable capital gain when they sell their Opportunity Fund investment, they would owe zero federal taxes on that capital gain.

Opportunity Fund investments may be held until December 31, 2047, which means that investors may be able to build decades of appreciation from any capital gains and owe nothing in capital gains tax on the earnings of the investment when they eventually sell it 10 or more years later.

Evaluating Your Options

So how do you determine which option is best for you?

It’s a tough question, and one that deserves thorough consideration, which should involve consulting with your personal tax or estate planning expert. But, there are a few basic guidelines that can help you navigate your options.

Real estate can offer many unique benefits, including attractive tax advantages. But how you invest in real estate can determine how many tax advantages you receive and the magnitude of those benefits. This is why it is important to weigh the costs and benefits of various tax incentive structures, and determine which is most suitable for your current portfolio and long-term goals.

I hope this helps you and your journey.