Financing options for a BRRRR + STR?

What are my financing options if I want to do a BRRRR + STR? I prefer to use conventional loan over DSCR for the refi due to lower rates and no prepayment penalty. Specifically:

- 1. Do I have to purchase the house and rehab using all cash to get around the 12 month loan seasoning requirement or are there hard money loans out there that can work (no mortgage on property)?

- 2. In order to get around the 6 month title seasoning requirement I have to meet the delayed financing exception. Under this exception, can the new loan amount fully cover initial purchase cost + rehab or only purchase cost?

- 3. Do conventional loans even allow STR or is it indifferent between LTR and STR?

I've read previous posts about this topic but some of them were dated prior to the 12-month loan seasoning requirement that was updated in April 2023, so wanted to confirm I'm understanding it correctly.

1. If you want to use conventional financing for the refinance, there is no way around the 12 month rule assuming you want to use the appraised value to determine LTV. Anything sooner than that would be based on purchase price.

2. The new loan amount would be based on the purchase price + closing costs, not rehab costs.

3. It all depends on whether or not the numbers work out. Much more to a conventional loan than a DSCR lon as far as qualification goes.

To address your other concerns - rates for DSCR loans aren't always that much higher than conventional, and prepayment penalities can be bought down. If you don't want to have to wait a year to pull your cash out of the property and base the new loan on the after rehab value, DSCR is your best option. Feel free to reach out if you have any other questions!

-

Broker Ohio (#NMLS 2339224)

- Barrett Financial Group, L.L.C.

- 330-354-6590

- [email protected]

- Attorney

- Philadelphia

- 670

- Votes |

- 472

- Posts

- Attorney

- Philadelphia

@Yvonne Wang. There is no regulation that mandates a set seasoning period. This is something that will be determined on a case by case basis by individual lenders. Some have seasoning requirements, others do not. There’s also plenty of lenders who will fund construction and provide for a stabilized release which works similarly to a cash out refinance. This is more difficult to secure in this high rate environment but so is a cash out refinance. However there are two other things to be mindful of:

1. I suspect this property is in Philadelphia based on where you pinned the post. Philadelphia introduced legislation at the beginning of 2023 that severely limits the ability to legally operate STR's in the city. Be certain your property has the correct zoning and licensing as most cannot meet the requirements to obtain the necessary licensure.

2. Expect your loan to be underwritten using an appraisal that is based on the markets long term rents, not the higher income you presumable expect to collect operating as a STR. Make sure this is factored into your valuation & underwritng. What most fail to realize is the STR model is more of a business operation whereas a lender cares about the fundamentals of the real estate. It's what they rely on as their collateral, not your STR business and the spread you can make relative to a traditional leasehold interest property.

-

Attorney

- Contract Assist

- [email protected]

@Brittany Minocchi Just to be clear the 12 month seasoning you mention is a Barrett Financial underwriting requirement, correct?

@Yvonne Wang Use this website to cross check for zoning and whether the permitting is in place.

http://atlas.phila.gov It's a good website with accurate reporting. I recently learned even the MLS can be slow to update and doesn't necessarily reflect the most up to date zoning.

Quote from @Sebastian Bennett:

@Brittany Minocchi Just to be clear the 12 month seasoning you mention is a Barrett Financial underwriting requirement, correct?

@Yvonne Wang Use this website to cross check for zoning and whether the permitting is in place.

http://atlas.phila.gov It's a good website with accurate reporting. I recently learned even the MLS can be slow to update and doesn't necessarily reflect the most up to date zoning.

No - it is a requirement for ALL conventional loans backed by Freddie/Fannie regardless of which lender you obtain the loan through.

-

Broker Ohio (#NMLS 2339224)

- Barrett Financial Group, L.L.C.

- 330-354-6590

- [email protected]

- Lender

- Austin, TX

I'm biased, but I don't think conventional is the best product if you are doing a rehab. You mention using hard money for the rehab, which, in combination with a conventional loan, would require you to be in high-interest rates for a year until you can cash out refinance. With some DSCR loans, you can cash out refinance in as little as three months, and the rest you need 6 months. With conventional, this would mean you would be paying 6-9 months of high-interest rate debt before you can pull cash out.

If you decide not to do a DSCR loan, the second home loan is a popular option, but there are lots of drawbacks for investors as it is really a product made for regular home buyers. With second home loans, the mortgage must be for one unit (I do a lot of 2-4 unit STRs), the property must not be rented for more than 180 days out of the year (limits revenue), must function reasonably as a second home (usually limits out of state investing), rental income will not qualify as stable monthly income (projected AirDNA does not play into your DTI). There are a couple others, but you can check the Freddie guidelines yourself:

https://guide.freddiemac.com/app/guide/section/4201.15

For AirBnBRRRRs, I suggest structuring with a hard money loan to purchase and rehab the property and then doing a DSCR refinance using AirDNA projections. This gives you the most flexibility with investment properties. Also if the prepayment and rates are a deal killer, you can always structure the deal with no prepayment or buy down the rate to the 6's.

@Brittany Minocchi Thanks for clarifying. This is interest subject material for me.

Quote from @Brittany Minocchi:

Quote from @Sebastian Bennett:

@Brittany Minocchi Just to be clear the 12 month seasoning you mention is a Barrett Financial underwriting requirement, correct?

@Yvonne Wang Use this website to cross check for zoning and whether the permitting is in place.

http://atlas.phila.gov It's a good website with accurate reporting. I recently learned even the MLS can be slow to update and doesn't necessarily reflect the most up to date zoning.No - it is a requirement for ALL conventional loans backed by Freddie/Fannie regardless of which lender you obtain the loan through.

@Brittany Minocchi thanks for the clarification. I read the Fannie seller guide and it says that a cash out refinance has a 12-month seasoning requirement if it is paying off an existing first mortgage: "If an existing first mortgage is being paid off through the transaction, it must be at least 12 months old at the time of refinance, as measured by the note date of the existing loan to the note date of the new loan." But I interpreted this seasoning requirement to not apply if there's no first mortgage on the property (initial purchase was all cash). https://selling-guide.fanniemae.com/sel/b2-1.3-03/cash-out-r... But you are saying even if there's no mortgage on the property / it was bought with cash initially any cash out refinance using Fannie/Freddie loans still require a 12 month seasoning period? Do you mind pointing me to where this requirement is in the selling guide?

Quote from @Yvonne Wang:

Quote from @Brittany Minocchi:

Quote from @Sebastian Bennett:

@Brittany Minocchi Just to be clear the 12 month seasoning you mention is a Barrett Financial underwriting requirement, correct?

@Yvonne Wang Use this website to cross check for zoning and whether the permitting is in place.

http://atlas.phila.gov It's a good website with accurate reporting. I recently learned even the MLS can be slow to update and doesn't necessarily reflect the most up to date zoning.No - it is a requirement for ALL conventional loans backed by Freddie/Fannie regardless of which lender you obtain the loan through.

@Brittany Minocchi thanks for the clarification. I read the Fannie seller guide and it says that a cash out refinance has a 12-month seasoning requirement if it is paying off an existing first mortgage: "If an existing first mortgage is being paid off through the transaction, it must be at least 12 months old at the time of refinance, as measured by the note date of the existing loan to the note date of the new loan." But I interpreted this seasoning requirement to not apply if there's no first mortgage on the property (initial purchase was all cash). https://selling-guide.fanniemae.com/sel/b2-1.3-03/cash-out-r... But you are saying even if there's no mortgage on the property / it was bought with cash initially any cash out refinance using Fannie/Freddie loans still require a 12 month seasoning period? Do you mind pointing me to where this requirement is in the selling guide?

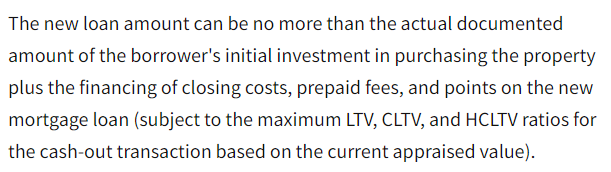

You are correct that the 12 month period applies if there is currently a mortgage on the property. However, if you are refinancing a property purchased with cash within 6 months of purchase, this is considered delayed financing. A cash out refinance and delayed financing are not exactly the same thing. While there isn't necessarily a 12 month seasoning requirement to refinance in this instance, your loan amount will be limited to the original purchase price + closing costs/fees/points if you refinance before the 12 month seasoning period has passed. So to clarify, the 12 month seasoning applies if you want to use the appraised value of the property. If you only want to pull your initial investment, then this would work. Most people who are completing rehab want to pull based on the value they have added to the property. See below for a snippet from the Selling Guide.

-

Broker Ohio (#NMLS 2339224)

- Barrett Financial Group, L.L.C.

- 330-354-6590

- [email protected]

Thanks for clarifying!